![]()

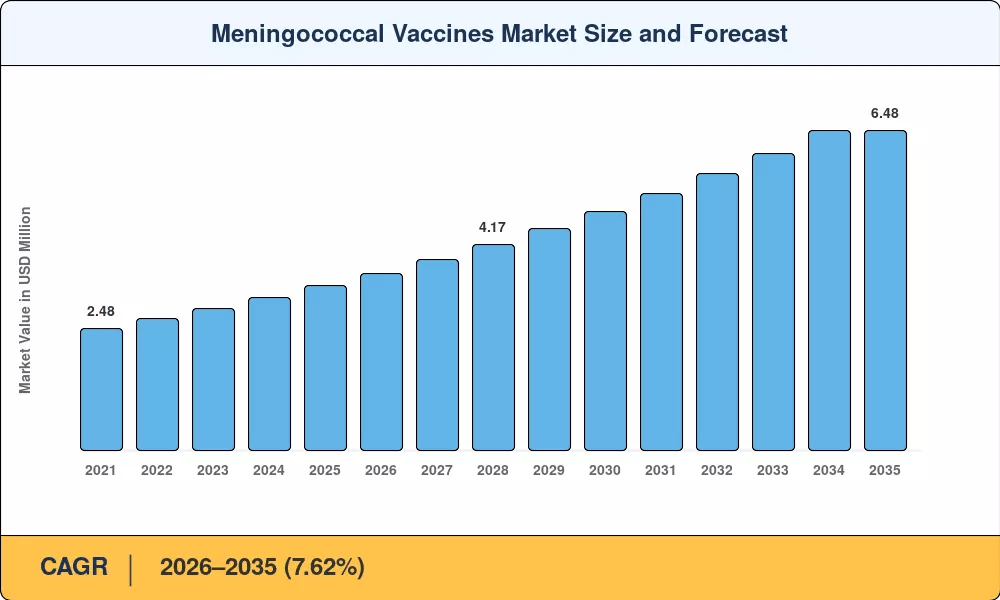

Meningococcal Vaccines Market to Surge from USD 3.59 Bn in 2026 to USD 6.48 Bn by 2035- By Pentavalent Platform Disruption, Meningitis Elimination Roadmap

NY, CA, UNITED STATES, June 16, 2026 /EINPresswire.com/ — As per Market Research Future, the global Meningococcal Vaccines Market size to reach USD 6.48 Billion by 2035 from USD 3.59 Billion in 2026, at a CAGR of 7.62% during the forecast period 2026–2035. The market base was estimated at USD 3.34 Billion in 2025.

The 7.62% CAGR—anchored by structural shifts in immunization schedules and global disease elimination commitments rather than episodic outbreak spending—is driven by three converging forces: the FDA approval of pentavalent platforms combining serogroups A, B, C, W, and Y in a single injection that is compressing multi-visit schedules and expanding series completion rates, the WHO’s Global Roadmap to Defeat Meningitis by 2030 which has mobilized over USD 450 million in Gavi co-financing for bacterial meningitis prevention campaigns across Sub-Saharan Africa and South Asia, and the expansion of mandatory adolescent meningitis vaccination requirements now covering 32 U.S. states and multiple European university systems.

Regulatory milestones and domestic manufacturing innovation are amplifying this momentum. GSK’s Penmenvy secured the first FDA clearance for a pentavalent conjugate meningococcal vaccine in February 2025, while Pfizer’s Penbraya followed closely—both cannibalizing older quadrivalent brands and triggering over USD 1.2 billion in cumulative R&D commitments from the top five manufacturers since 2023.

The Serum Institute of India’s WHO-prequalified Men5CV, priced below USD 3 per dose for Gavi-eligible countries, positions South Asia as both a high-growth consumer and a global low-cost manufacturing hub for Neisseria meningitidis immunization. These technology, policy, and access forces together are creating the procurement infrastructure on which the Meningococcal Vaccines Market depends.

Request A Free Sample: https://www.marketresearchfuture.com/sample_request/8622

Key Market Trends & Growth Drivers

Pentavalent Platform Disruption

GSK’s Penmenvy approval in February 2025 marked a watershed for the Meningococcal Vaccines Market. By packaging serogroups A, B, C, W, and Y into a single conjugate meningococcal vaccine, the product eliminates what was previously a two- or three-visit adolescent meningitis vaccination schedule. CDC estimates suggest a single-visit pentavalent regimen could lift series completion rates from 57% to over 78% among U.S. 16-year-olds, translating into incremental procurement volume of approximately 8 million doses annually.

Pfizer’s Penbraya, approved in October 2023 as the first pentavalent vaccine on the U.S. market, established the commercial blueprint that GSK has now followed with a competing formulation. Together, these launches have triggered a fundamental reconfiguration of hospital and pharmacy formularies and compressed the multi-product adolescent schedule into a more adherence-friendly single-appointment model.

WHO 2030 Meningitis Elimination Roadmap and Global Funding

The WHO’s Global Roadmap to Defeat Meningitis by 2030 has catalyzed coordinated financing across 26 high-burden nations, transforming sporadic outbreak-response procurement into sustained routine Neisseria meningitidis immunization programs. Gavi’s March 2024 allocation of USD 200 million targets 80 million doses across 15 Gavi-eligible countries by 2027, while a funded emergency stockpile of multivalent meningococcal vaccines secures supply continuity during meningitis belt epidemic seasons.

The Serum Institute of India’s Men5CV—WHO-prequalified in 2024 and produced at under USD 3 per dose—directly addresses the cold-chain and cost barriers that historically prevented sustained bacterial meningitis prevention in Sahel nations. This roadmap creates guaranteed multi-year purchase commitments that de-risk manufacturer capacity investments across the forecast period.

Expanded Adolescent Mandates and Outbreak-Driven Demand

Thirty-two U.S. states now require at least one dose of MenACWY for school admission, and more than a dozen states or university systems require serogroup B meningococcal protection or explicit risk disclosures for college enrollment—converting adolescent meningitis vaccination into a reliable, recurrent revenue stream for manufacturers.

Similar frameworks are emerging in Australia and several Western European regions. Simultaneously, the rising incidence of serogroup W and Y invasive meningococcal disease in Chile, Argentina, and Saudi Arabia has prompted emergency supplementary immunization campaigns: Chile alone procured 1.4 million additional MenACWY doses outside its routine schedule between 2022 and 2024, illustrating how outbreak patterns create non-linear demand spikes that add revenue beyond routine schedule volumes.

Ask for Customization: https://www.marketresearchfuture.com/ask_for_customize/8622

Market Segment Insights

BY PRODUCT TYPE

Quadrivalent Vaccines: Dominant segment at ~57% revenue share (2025). Products like Menveo and Menactra hold deep formulary positions built on long-standing ACIP and EMA adolescent meningitis vaccination mandates. Their installed base across 32 U.S. state school-entry requirements means market erosion toward pentavalent alternatives will be gradual, driven by formulary committee decisions and reimbursement parity timelines.

Pentavalent Vaccines: Fastest-growing product type at 9.10% CAGR (2026–2035). Expected to capture over 35% of global doses by 2030, up from under 5% in 2025. GSK’s Penmenvy and Pfizer’s Penbraya are driving this shift by consolidating multi-dose schedules and improving series completion rates, with manufacturer combined share projected to exceed 45% by decade-end.

Bivalent Vaccines: Growing at 8.59% CAGR (2026–2035). Bexsero and Trumenba target serogroup B meningococcal protection—the fastest-growing legacy category fueled by rising awareness of serogroup B outbreaks on U.S. college campuses and ACIP Category A recommendations that have shifted these products from discretionary to near-routine purchases.

Monovalent Vaccines: Accounted for USD 0.28 Billion (2025). Primarily serves meningitis belt MenA mass campaigns and Hajj-mandate travel vaccination. Volumes will gradually rationalize as Men5CV pentavalent platforms provide broader serogroup coverage at competitive cost in the same high-burden settings.

BY VACCINE TYPE

Conjugate Vaccines: Dominant at 49% share (2025). Superior T-cell-dependent immune memory lasting 5–10 years versus the 3–5-year duration of polysaccharide alternatives makes conjugate meningococcal vaccine technology the preferred platform for routine infant and adolescent programs globally. The shift toward conjugate technology in Gavi-eligible markets is a structural, multi-decade transition.

Combination Vaccines: Fastest-growing type at 8.72% CAGR. Pentavalent platform adoption consolidating conjugate and recombinant protein antigens represents the next frontier of Neisseria meningitidis immunization. Co-packaged regimens pairing meningococcal antigens with HPV or Tdap boosters improve visit efficiency and appeal to health systems focused on reducing per-encounter costs.

Recombinant Protein Vaccines: Growing at 7.95% CAGR. MenB-specific antigen targeting through recombinant platforms underpins serogroup B meningococcal protection products. Moderna and BioNTech are additionally exploring mRNA-based meningococcal candidates that could enable rapid strain-matched updates analogous to seasonal influenza vaccines by the early 2030s.

Polysaccharide Vaccines: Contributed USD 0.52 Billion (2025). Remain cost-effective for outbreak response procurement and in settings where cold-chain maturity and budget constraints preclude full conjugate transition. Volumes declining structurally as conjugate alternatives achieve price parity through Gavi tiered purchasing.

BY SALES CHANNEL

Public Sector: Dominant at 72% share (2025). Government NIP procurement, Gavi alliance tenders, and PAHO revolving fund access collectively represent the primary revenue channel. Guaranteed multi-year purchase commitments from Gavi’s next replenishment cycle (2026–2030)—expected to allocate over USD 600 million to bacterial meningitis prevention—de-risk manufacturer capacity investments and sustain public-sector volume throughout the forecast period.

Private Sector: Fastest-growing channel at 8.78% CAGR. Parents in high-income countries are increasingly seeking out-of-schedule serogroup B meningococcal protection for adolescent children entering university, and travel vaccination demand for pilgrims and adventure travelers adds a stable premium-priced revenue stream. The private channel’s faster growth reflects pentavalent premium pricing that is absorbed more readily by commercially insured patients.

BY AGE GROUP

Children & Adults (≥2 years): Dominant at 80% share (2025). School-entry and adolescent mandates across North America and Europe generate a reliable, policy-anchored demand base. Hajj-linked adult vaccination in Saudi Arabia and travel medicine demand among adult populations add predictable seasonal volume.

Infants (0–2 years): Fastest-growing cohort at 8.82% CAGR. Expanded infant NIP inclusion—already active in the UK since 2015, Brazil since 2020, and under evaluation in India’s Universal Immunization Programme—represents the highest-volume long-term growth vector. India’s potential UIP inclusion alone could add 26 million annual doses for conjugate meningococcal vaccine programs.

Read Detailed Insights: https://www.marketresearchfuture.com/reports/meningococcal-vaccines-market-8622

Regional Outlook

North America — Dominant Market (~43% Share, 2025)

The United States generates approximately 82% of North American Meningococcal Vaccines Market revenue, accounting for over USD 1.17 billion in annual spending. Mandatory school-entry MenACWY requirements across 32 states, robust commercial insurance reimbursement, and ACIP’s expanded serogroup B meningococcal protection recommendations for college-aged populations together create the deepest and most policy-durable demand base globally.

Pentavalent launches are expected to compress the current two-product adolescent schedule into a single visit, lifting series completion rates by an estimated 12–15% in volume terms by 2028. Canada is growing at 7.48% CAGR as provinces harmonize adolescent meningitis vaccination protocols with U.S. AHA/ASA–aligned guidelines. Mexico contributes USD 0.04 Billion through Secretaría de Salud routine schedule additions targeting urban pediatric populations.

Europe — Second Largest (~27% Share, 2025)

Europe’s Meningococcal Vaccines Market benefits from the UK’s pioneering 2015 infant serogroup B meningococcal protection program—now a global template replicated in France, Italy, and Spain—and the European Commission’s 2024 joint procurement directive expected to standardize pricing across 27 member states. The UK contributes 22% of European revenue, energized by the NHS commitment to full national MenB infant coverage. Germany contributes USD 0.14 Billion on STIKO recommendations and public reimbursement.

France is growing at 7.35% CAGR on expanded adolescent serogroup B meningococcal protection reimbursement. Spain is growing at 8.10% CAGR on strong private-market parental demand for MenB vaccines. Sanofi’s USD 180 million capacity expansion at its Marcy-l’Étoile facility, announced June 2024, directly supports MenQuadfi production scale-up for EU joint procurement tenders, signaling confidence in European volume growth.

Asia-Pacific — Fastest-Growing Region (8.92% CAGR, 2026–2035)

Asia-Pacific is the engine of the Meningococcal Vaccines Market, representing both the largest addressable population opportunity and the most important low-cost manufacturing hub for global Neisseria meningitidis immunization.

China holds 32% of regional revenue, with CDC schedule expansion and domestic biosimilar production driving competitive pricing that is penetrating public hospital systems. India is growing at 9.25% CAGR—the highest country-level rate—propelled by UIP evaluation for conjugate meningococcal vaccine inclusion in an annual birth cohort of approximately 25 million infants; inclusion alone could add 26 million doses per year.

Middle East & Africa — High-Need Frontier (USD 0.21 Billion, 2025)

Saudi Arabia leads the MEA Meningococcal Vaccines Market at 28% of regional revenue, underpinned by the world’s most uniquely predictable demand spike: mandatory Hajj vaccination requirements that vaccinate over 2 million international pilgrims annually, concentrating roughly 6% of global meningococcal doses into a 10-week procurement window each year. The UAE is growing at 8.05% CAGR on medical tourism and expatriate health mandates.

South America — Growing Presence (USD 0.17 Billion, 2025)

Brazil anchors South America’s Meningococcal Vaccines Market at approximately 54% of regional revenue through the Unified Health System (SUS), which added MenACWY to the infant schedule in 2020 creating a stable public-sector demand base. Argentina is growing at 7.90% CAGR, driven by the country’s ongoing response to a persistent serogroup W outbreak since 2019 that has pushed supplementary adolescent meningitis vaccination campaigns well above routine schedule levels.

Competitive Landscape and Recent Developments

The Meningococcal Vaccines Market exhibits medium concentration, with an estimated HHI of approximately 2,200 and the top five players controlling roughly 72% of global revenue. GSK and Pfizer lead through their pentavalent platforms, Sanofi maintains a strong legacy quadrivalent position, and the Serum Institute of India is disrupting pricing norms through high-volume low-cost production at less than one-tenth the unit cost of branded pentavalent alternatives.

The competitive structure is shifting rapidly: mid-tier manufacturers lacking pentavalent technology face margin compression and are being forced to license next-generation platforms or rationalize product portfolios. The landscape is stratified between broad-portfolio global vaccine leaders, emerging-market manufacturing champions, and early-stage mRNA and recombinant protein platform entrants.

KEY COMPANIES AND RECENT MILESTONES

GSK plc (February 2025): Received FDA approval for Penmenvy, covering serogroups A, B, C, W, and Y in a single conjugate meningococcal vaccine—the first pentavalent product combining Bexsero and Menveo components. Commands an estimated 18–22% global revenue share, with first-mover pentavalent advantage and dominant positioning in infant serogroup B meningococcal protection through the Bexsero franchise.

Pfizer Inc. (October 2023): Received FDA approval and launched Penbraya as the first pentavalent meningococcal vaccine on the U.S. market, targeting the adolescent meningitis vaccination segment with a two-dose schedule covering serogroups A, B, C, W, and Y. Holds an estimated 16–20% global revenue share through its combined Penbraya, Trumenba, and Nimenrix portfolio.

Sanofi S.A. (June 2024): Announced a USD 180 million capacity expansion at its Marcy-l’Étoile facility to support MenQuadfi production scale-up for EU joint procurement tenders, reinforcing its 14–18% revenue share legacy quadrivalent leadership position while it evaluates pentavalent pipeline strategy.

Serum Institute of India (2024): Achieved WHO prequalification for Men5CV (NmCV-5), a pentavalent meningococcal vaccine covering serogroups A, C, W, Y, and X priced below USD 3 per dose for Gavi-eligible countries—approximately one-tenth the cost of branded alternatives. Holds 6–9% global revenue share and is positioned as the manufacturing hub for Sub-Saharan African Neisseria meningitidis immunization campaigns.

Future Outlook: 2026–2035

By 2030, pentavalent meningococcal vaccines are expected to capture over 35% of global doses, up from under 5% in 2025, fundamentally restructuring the Meningococcal Vaccines Market competitive landscape. Mid-tier manufacturers lacking pentavalent technology will face margin compression and be forced to license next-generation platforms or exit the market entirely. GSK and Pfizer are projected to control combined share exceeding 45% by decade-end, reinforced by the clinical evidence base, formulary entrenched positions, and supply-chain advantages that flow from being first-mover in the pentavalent space.

mRNA technology extension to meningococcal antigens represents the most transformative long-term opportunity. Moderna’s Phase II candidate targeting serogroups B and X, if successful, could enable rapid strain-matched updates analogous to seasonal influenza vaccine reformulation—creating recurring annual revenue cycles and dramatically accelerating response to emerging serogroup epidemics.

If regulatory agencies establish an expedited pathway for meningococcal strain updates by 2030, the mRNA-based conjugate meningococcal vaccine development model could attract new entrants and fundamentally compress the product lifecycle economics of the industry. Clinical licensure of mRNA-based meningococcal products before 2033 is considered unlikely, however, meaning conjugate and recombinant protein platforms will dominate commercial volumes throughout most of the forecast period.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/vaccine-research-market-27935

https://www.marketresearchfuture.com/reports/recombinant-vaccines-market-6130

https://www.marketresearchfuture.com/reports/pediatric-vaccines-market-5779

https://www.marketresearchfuture.com/reports/human-vaccines-market-2671

https://www.marketresearchfuture.com/reports/infectious-disease-treatments-market-1626

https://www.marketresearchfuture.com/reports/conjugate-vaccine-market-4387

https://www.marketresearchfuture.com/reports/hepatitis-vaccine-market-32320

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery